By: Charles_Carnevale

By now, it should be no secret to anyone that the stock market has been on a nice run of late. Moreover, this Bull Run has conjured up a lot of discussions that might lead one to believe that stocks in general are overvalued.? There are even some that want to play the bubble card because they argue that the S&P 500 and/or the Dow Jones Industrial Average are both approaching all-time highs. However, I believe these extremists are confusing value with price.

By now, it should be no secret to anyone that the stock market has been on a nice run of late. Moreover, this Bull Run has conjured up a lot of discussions that might lead one to believe that stocks in general are overvalued.? There are even some that want to play the bubble card because they argue that the S&P 500 and/or the Dow Jones Industrial Average are both approaching all-time highs. However, I believe these extremists are confusing value with price.

Investors need to understand and recognize that both a company and/or an index can be trading at an all-time high price, while at the same time be trading at a reasonable or even a low valuation.? Additionally, there can be more than one reason for this to occur. For example, if earnings are at an all-time high, the price can also be at an all-time high while the PE ratio is lower than historical norms. Another iteration can manifest because the stock or index was once previously trading at an extreme overvaluation, while it is now fairly valued.

My point is that it is not logical to automatically assume that a stock is overvalued because it is trading at its highest price ever.? If earnings growth has also been strong, it is possible that even at its current highest price ever, that the stock is undervalued or fairly valued. For the sake of their long-term performance, it is important that investors understand this distinction, recognize it, and make investment decisions based more on true value than on price.

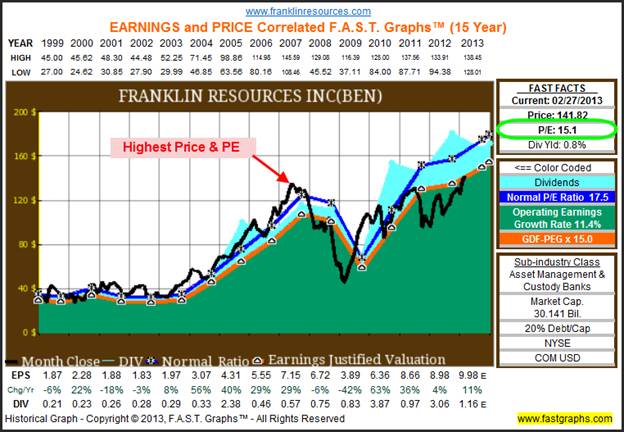

Currently, I can cite four high profile Dividend Aristocrats that are in this situation: 1. Franklin Resources (BEN) 2.? Illinois Tool Works (ITW) 3.? Johnson & Johnson (JNJ) 4.? 3M Corp. (MMM). ?The following historical earnings and price correlated FAST Graphs? on Franklin Resources illustrates my point. Franklin Resources is trading close to its highest price ever, but its current PE ratio of 15 indicates that it is currently fairly valued. In 2007 when its stock price was over $145 per share, its PE ratio was also over 20, and one of the highest PEs that Franklin Resources has ever been awarded.

The Relative Valuation of the Prestigious Standard & Poor?s Dividend Aristocrats

With this article, I am going to review the prestigious Standard & Poor?s Dividend Aristocrats list comprised of 51 blue-chip companies that have increased their dividend every year for 25 or more consecutive years. Furthermore, all of the Dividend Aristocrats are also included in David Fish?s Dividend Champions list comprised of 105 companies that likewise have increased their dividends every year for 25 consecutive years. An update of David?s CCC list can be found here.

However, the reason I chose the Dividend Aristocrats list is simply because not only is it a smaller list, but because I also believe it represents the cr?me de la cr?me of companies with a long streak of dividend increases.? But even more importantly, I believe this blue-chip list of dividend growth stocks represents the foundational choices that dividend growth investors in or contemplating retirement can depend on as income producers that offer the potential for a raise in pay each year.

Moreover, there have been two strong factors that cause me to generally favor these prestigious blue-chip dividend growth stocks since the great recession of 2008.? First of all, after the recession, most of these companies became historically undervalued even though their earnings held up for the most part, and of course their dividends continued to grow.? This created a real opportunity for the dividend growth investor to receive an above-average total return, and an above-average current dividend yield while simultaneously enjoying a higher margin of safety than normal valuations typically provide.

Although the recent run-up in stock prices over the past few years has partially closed this incredible window of opportunity, it has not completely slammed it shut.? As I will illustrate, extreme bargains are now harder to come by than they were just a few years ago, but there still are bargains to be had if investors are willing to dig deep enough. On the other hand, there are not as many bargains to be found today as there were just a few years ago. But this does not mean that there are not any good investments available. Companies that can be purchased at fair value are also good investments.

In other words, I believe there are still plenty of reasonably priced Dividend Aristocrats available.? Although we all love a bargain, we also have to realize that regarding investing in common stocks, we also have to accept what the marketplace is offering us in present time.? Nevertheless, I must admit to lamenting about all of the great bargains disappearing.? Today, I have to be willing to accept sound investments, also known as fairly valued investments, to invest current monies. To repeat, the truth is that if a company is at fair value it may not be a great bargain, but it still can be a sound and attractive investment.

In order to come to these conclusions, I have reviewed all of the 51 Dividend Aristocrats, one company at a time, in order to ascertain the relative valuation of each individual Dividend Aristocrat.? My research came up with seven companies out of the 51 that I considered bargains.? I felt that 16 were fairly valued, with an additional 18 that I considered only moderately overvalued.

It?s important to state here that valuation is not a precise measurement.? Therefore, I?m comfortable in saying that 31 of the 51 Dividend Aristocrats could be potential candidates for current investment. However, more comprehensive due diligence is indicated.? Also, I wrote extensively on the subject of sound valuation in my last article found here. ?

Additionally, I took some solace in the fact that my research only uncovered 10 Dividend Aristocrats that I considered dangerously overvalued. This is important, because a strong market like we have recently experienced can easily convince people that stocks have become overvalued. I believe it is vitally important to make investment decisions based on fact rather than innuendo. The key is to make the distinction between price and value.

Aristocrat Bargains

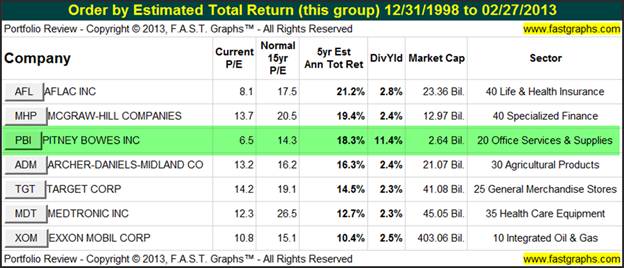

The following lists the seven Dividend Aristocrats that statistically appear to be trading at bargain valuations.? One way to measure this, as I have done in the following table, is to compare the current P/E ratio of the company to its historical normal P/E.?? However, as I will soon illustrate, statistics do not always tell the whole story, and sometimes not even enough of the story to make a rational decision.

Pitney Bowes Inc. (PBI) a Bargain or a Trap?

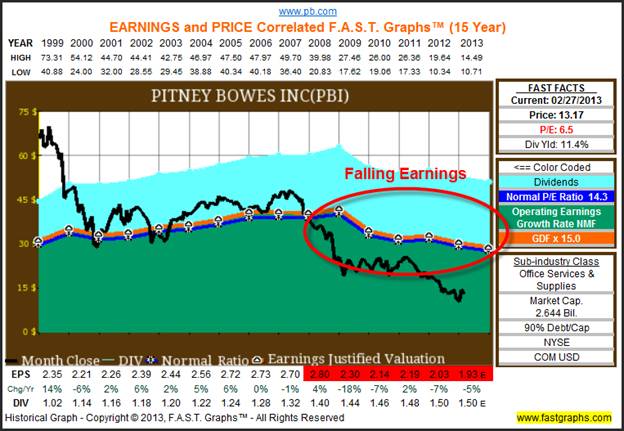

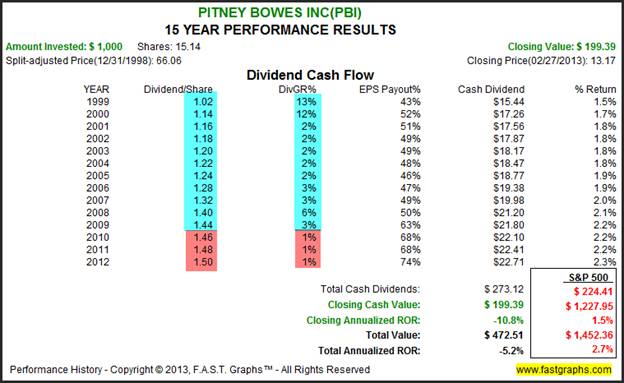

Statistically speaking, Pitney Bowes Inc. looks like a screaming bargain.? Its current PE ratio of 6.6 is less than half of its normal PE ratio of 14.3.? Moreover, its current dividend yield is over 11%.? Remember, this is a Dividend Aristocrat that has increased its dividend every year for 25 consecutive years (30 to be exact). These are all great statistics.? However, a closer look reveals some significant potential dangers that are lurking.

The moral of the story is that I believe prudent investing must go beyond gazing at spreadsheets or simply reviewing data points. It is possible, that Pitney Bowes is capable of turning its business around.? However, there is no substitute for comprehensive due diligence. Regarding Pitney Bowes, an article in Barron?s entitled Pitney Bowes' Enticing 10.8% Yield, may shed some light on this company?s future.

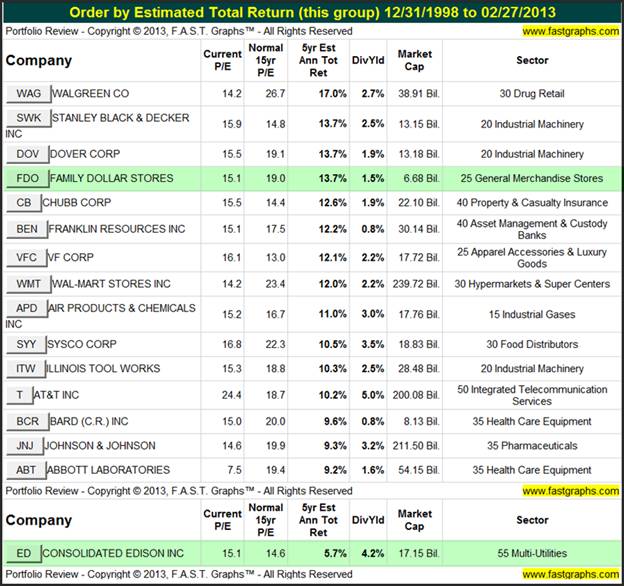

Aristocrats at Fair Value

This next table lists the 16 Dividend Aristocrats that appeared to be currently fairly valued.? Statistically speaking, each of the 16 candidates appears to be reasonably valued.? However, it?s important to remember that rather than a precise measurement, valuation is always indicated as a range of reasonableness.? Moreover, I consider fair valuation a measure of soundness and not necessarily an indicator of a high future return.

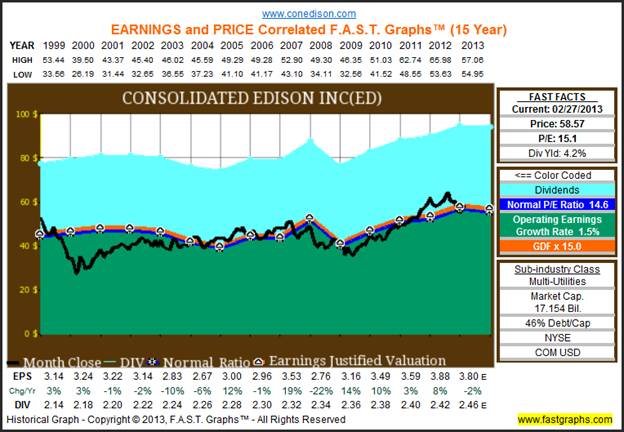

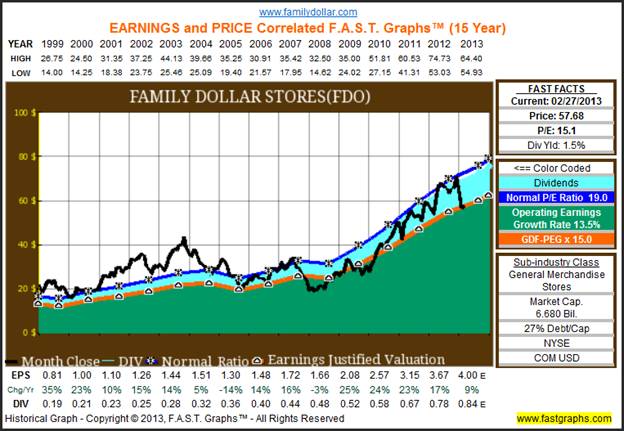

Consolidated Edison (ED) versus Family Dollar Stores (FDO)

The following specific examples from my fair value list illustrate how two companies that are both fairly valued can potentially offer entirely different potential future returns.? Consolidated Edison is a very slow growth utility stock that offers an attractive dividend yield but very little capital appreciation potential.

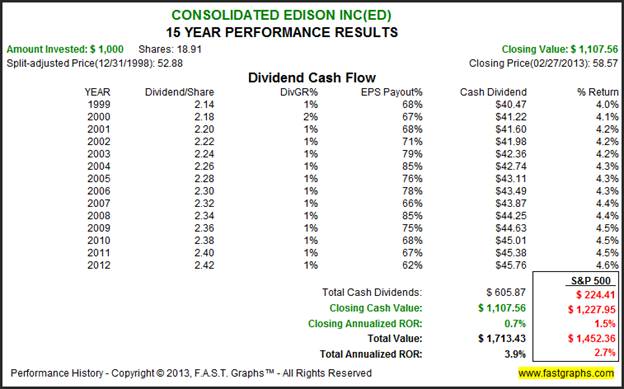

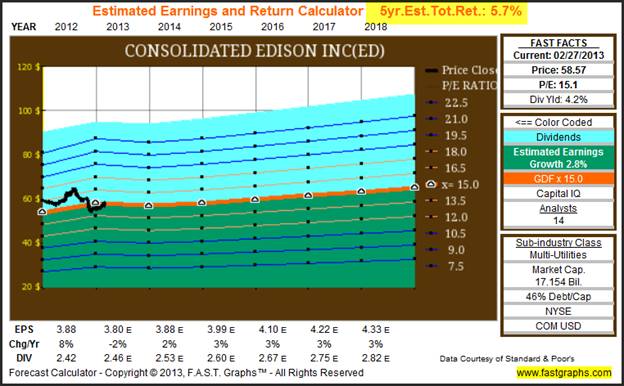

The following estimated earnings and return calculator based on the consensus of 13 analysts reporting to Capital IQ indicate that Consolidated Edison?s 5-year estimated total return would be 6.7%. ?However, it?s important to point out that the majority of this return would come from dividends, not growth.

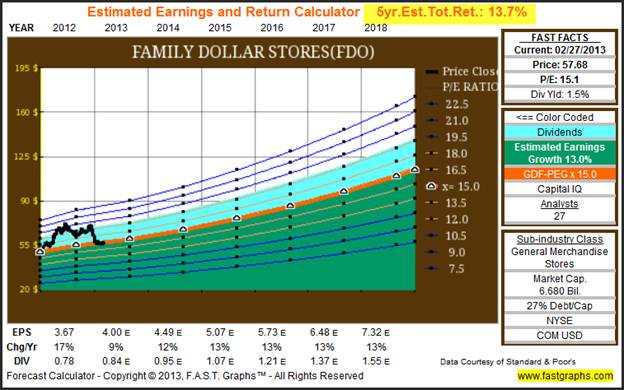

In contrast, Family Dollar Stores is a Dividend Aristocrat that can be purchased at a lower PE ratio than Consolidated Edison and also offers a much lower yield.? However, the major differentiator with Family Dollar versus Consolidated Edison is Family Dollars? historical and future growth potential.

The consensus forecast earnings growth by 27 analysts reporting to Capital IQ is 13% per annum. ?This number is very consistent with the company?s historical growth rate which might indicate that it is at least possible. Consequently, assuming that the company achieves this forecast earnings growth rate and trades at a fair value PE ratio, its future five-year estimated total return would be 14.6%.

Although both of the above sample companies are fairly valued, the potential future returns are materially different.? Fair valuation is a very important component of soundness and future return.? However, the primary driver of total future return, if fair value is in effect, will be the future earnings (and dividend) growth rate of the respective individual company.

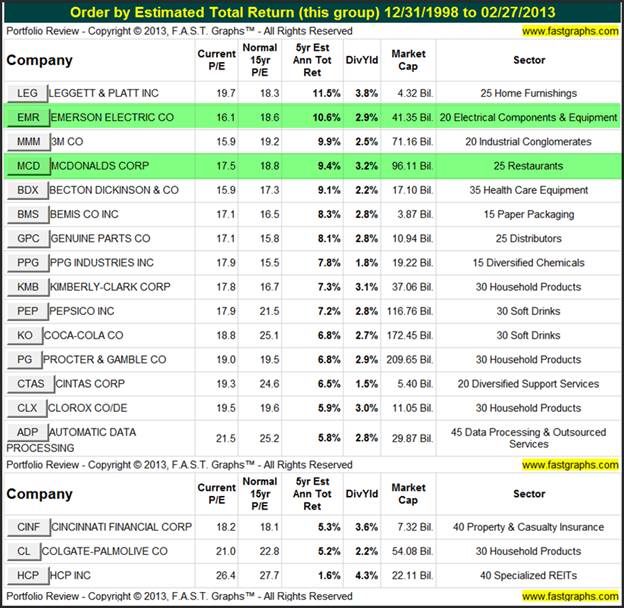

Aristocrats Moderately Overvalued

The following group of 18 Dividend Aristocrats I considered moderately overvalued still represent a potentially fertile field of investment choices.? First of all, what appears to be moderate overvaluation may, in fact, be fair valuation if forecasts for future growth are too conservative or understated. Of course, the opposite could also be true.

The next reason I believe this list could prove to be fertile ground is because even a small pullback in the share prices of most of these companies could easily move them back into fair value territory. Consequently, it would be in the best interest of prospective investors to look deeper into the possibilities of any of these apparently moderately overvalued Dividend Aristocrats.

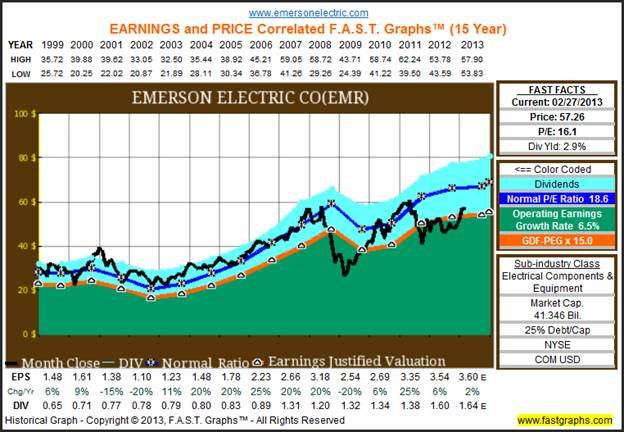

Emerson Electric (EMR)

A review of the following earnings and price correlated graph on Emerson Electric shows that the price is just barely above the orange earnings justified valuation line.? Consequently, prospective investors could perhaps comfortably start building positions at these levels, or perhaps wait for a small pullback. Nevertheless , Emerson Electric is far from being dangerously overvalued.

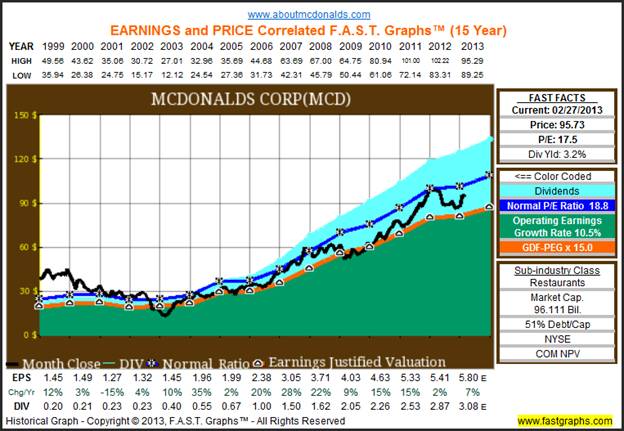

McDonald?s Corp. (MCD)

McDonald?s Corp. is a perennial favorite of the dividend growth investor.? Note by reviewing the following earnings and price correlated graph that this blue-chip Dividend Aristocrat often trades at a premium to its earnings justified valuation (the orange line). Consequently, this presents a dilemma for the dividend growth investor with money to invest.? Should I wait for a pullback, or should I go ahead and start building a position now before the price completely runs away from me?

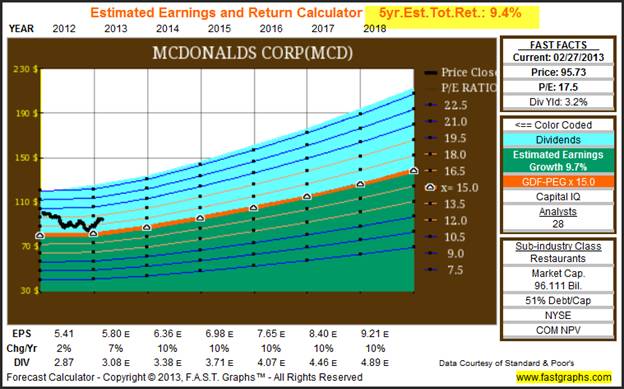

I believe that it is important to point out that McDonald?s still represents a potentially attractive long-term investment even at its current moderately overvalued level. The consensus of 28 analysts reporting to Capital IQ, expect McDonald?s to grow earnings at 9.7% per annum over the next five years.? Since this number is only slightly lower than McDonald?s historical normal growth, it also seems plausible.?

Therefore, a five-year estimated total return of 9.4% should satisfy most investors.? Moreover, this return assumes those earnings achievements are reached, and that McDonald?s trades at a fair value PE of only 15, which is lower than its current PE of 17.5.

Aristocrats Dangerously Overvalued

As previously mentioned, I only came across 10 of the 51 Dividend Aristocrats that I considered dangerously overvalued.? To me this means that the potential losses that would occur if the company?s share price moved back into fair value range are too high to absorb or be mitigated by any potential dividend increases. Another way that I think of this is to calculate how many years that I feel the stock price is ahead of current earnings.? I?ll illustrate this point more clearly later.

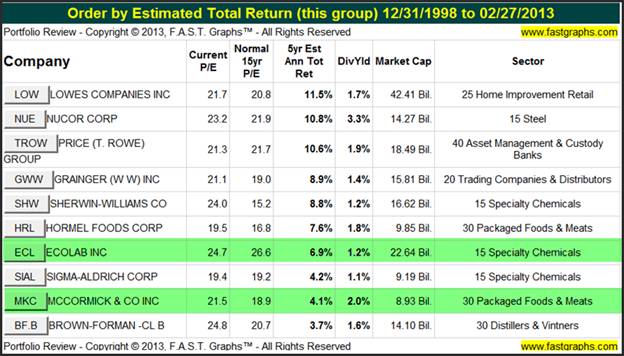

There is also a very interesting twist that I observed with several of these so-called overvalued Dividend Aristocrats. Only 5 of the 10 Dividend Aristocrats that I consider dangerously overvalued are priced above what the market has normally valued their shares at.? These are: 1.? McCormick & Co. (MKC) 2.? Sherman-Williams Co. (SHW) 3.? Hormel Foods Corp. (HRL) 4. W.W. Grainger (GWW) 5. Brown-Foreman CL B (BF.B).

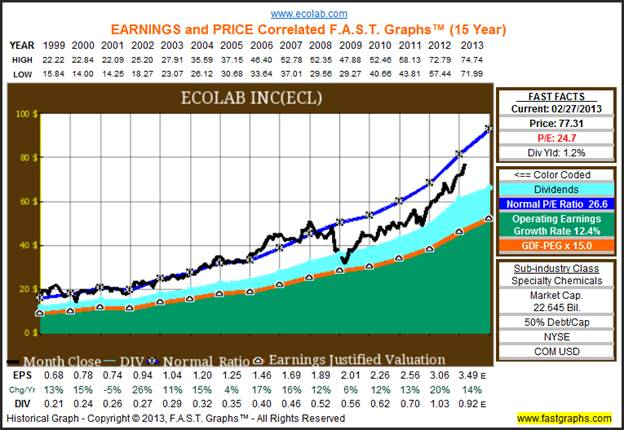

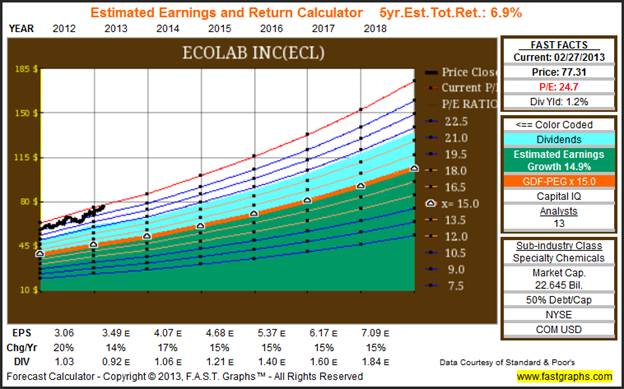

The other five Dividend Aristocrats are companies that the market has historically priced at a premium valuation.? Currently, these companies are trading at their normal premium valuation.? Therefore, an argument could be made that these companies are actually fairly valued on that basis.? Later I will provide an earnings and price correlated graph on Ecolab Inc. (ECL) that shows that this highly valued company may actually be slightly undervalued based on historical norms.

Ecolab ? overvalued or undervalued?

The earnings and price correlated graph on Ecolab Inc. clearly shows that the market has historically valued the shares at a normal PE ratio of 26.7 (the blue line) which is significantly above the earnings justified valuation PE of 15. In truth, a case could also be made that the company is currently undervalued based on its current PE of 24.7, which is below its normal PE of 26.7.

Nevertheless, this is a fact that could be taken into consideration by prospective investors that are really fond of this high-quality above-average dividend growth stock.? On the other hand, more cautious investors, like yours truly, would never be willing to pay up even for the consistency and quality that this company possesses. These kinds of judgments are left up to the individual investors? own risk tolerances and beliefs. On the other hand, making the decision with your eyes wide open based on the facts as presented is rational, if not prudent.

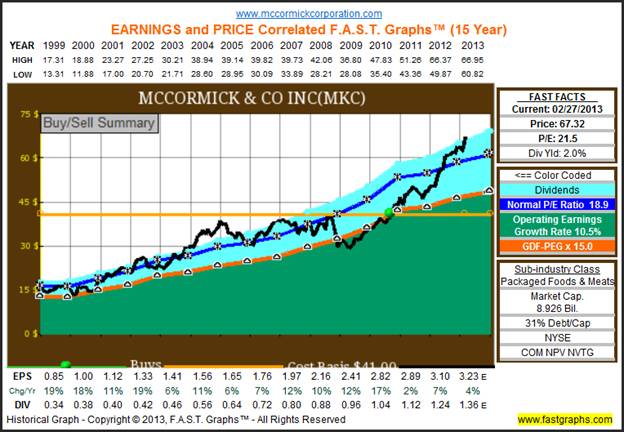

McCormick & Co. Inc. Clearly Dangerously Overvalued

When you review the earnings and price correlated graph on McCormick & Co. you also discover that the market has often placed a premium valuation on its shares. However, current valuation is clearly above even the premium valuation that the market has often applied.? Therefore, I believe that new purchases in McCormick & Co. should be avoided unless the shares pull back.

Consistent with full disclosure, we are long McCormick & Co.? Moreover, I submit that is one of my favorite dividend growth stocks for many reasons.? However, I was only willing to purchase this company when its stock price was trading at what I considered to be fair value.? The following graph is marked with a green dot where I purchased McCormick & Co., and the yellow line represents my cost basis.? Sadly, I?ve now placed McCormick & Co. on my potential sell list due to its high valuation.? This is one of those disappearing bargains that I lamented about earlier.

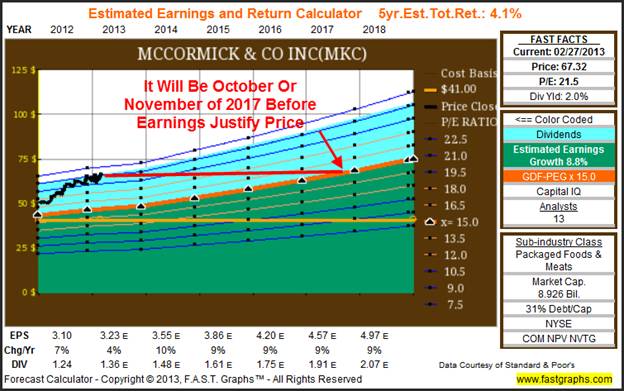

As promised earlier, the following estimated earnings and return calculator shows how I calculate how many years that I feel the current price is ahead of earnings justified levels. More clearly stated, if current earnings expectations are correct, future earnings would not justify today?s valuation until October or November of 2017.? Even though I could rationalize that the stock is only modestly ahead of its historically normal PE ratio, I am not willing to take that risk.

Summary and Conclusions

As I?ve written many times in the past, I am not too concerned with trying to forecast the stock market in the general sense.? I believe that it is a market of stocks, rather than a stock market.? Moreover, my observations spaning over many decades have provided me conclusive evidence that it is more rational to evaluate individual stocks than it is to worry about the general state of the market, or the economy for that matter. My experience has taught me that in every market, whether it be a bull market or a bear market, there will be individual stocks that are overvalued, fairly valued or undervalued.

Therefore, I believe that stock portfolios should be built one company at a time, and specifically based on the individual merits of each respective stock. As a result, I don?t worry too much about the markets or the economy in general, but instead I focus my energies and attention on analyzing each individual company that I may be interested in owning.? On the other hand, by assessing fair value within a reasonable degree of accuracy, I am relieved of the wasted effort of wasting my time on stocks that are clearly outside of my buying parameters.

As I write this article, I do believe that most of the great bargains created by the Great Recession of 2008 are now gone.? On the other hand, that doesn?t mean that there are no longer any good buying opportunities out there.? Quite the contrary, I continue to believe that the majority of the blue-chip Dividend Aristocrats are worthy of serious consideration.? Moreover, I believe that investors could get aggressive with these blue chips if any pullback were to occur.? This is especially true of companies whose earnings and dividends continue to advance in spite of falling stock prices.

Finally, I believe that investors need to always be making decisions that are as rational as they can be based on facts and not false assumptions.? This reminds me of a favorite Will Rogers? quote regarding how we learn.? He said there are three strategies people use to learn:? ?The ones that learn by reading. The few who learn by observation. The rest that have to pee on the electric fence and find out for themselves.?

Disclosure:? Long ITW, JNJ, MCD, EMR, MKC at the time of writing.

By Chuck Carnevale

http://www.fastgraphs.com/

Charles (Chuck) C. Carnevale is the creator of F.A.S.T. Graphs?. Chuck is also co-founder of an investment management firm.? He has been working in the securities industry since 1970: he has been a partner with a private NYSE member firm, the President of a NASD firm, Vice President and Regional Marketing Director for a major AMEX listed company, and an Associate Vice President and Investment Consulting Services Coordinator for a major NYSE member firm.

Prior to forming his own investment firm, he was a partner in a 30-year-old established registered investment advisory in Tampa, Florida. Chuck holds a Bachelor of Science in Economics and Finance from the University of Tampa. Chuck is a sought-after public speaker who is very passionate about spreading the critical message of prudence in money management. Chuck is a Veteran of the Vietnam War and was awarded both the Bronze Star and the Vietnam Honor Medal.

? 2013 Copyright Charles (Chuck) C. Carnevale - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

? 2005-2013 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.

Source: http://www.marketoracle.co.uk/Article39276.html

2012 dunk contest edgar vs henderson berkshire hathaway ufc 144 james jones james jones aladdin

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.